India’s eCommerce sector has emerged as one of the world’s fastest-growing digital marketplaces, with a market size of $147.3 billion in 2024 and a projected compound annual growth rate (CAGR) of 18.7% through 2028. The market is expected to reach 400 million consumers by 2027, up from 312.5 million in 2022. This rapid expansion is driven by increasing internet penetration (690 million users representing 40% of the population), growing smartphone adoption, cheaper data rates, and expanding reach into Tier II and III cities.

The Indian eCommerce landscape is characterized by significant market concentration in horizontal marketplaces, complemented by a vibrant ecosystem of vertical specialists and emerging quick commerce platforms. Below is an analysis of the top 15 companies reshaping India’s digital commerce landscape.

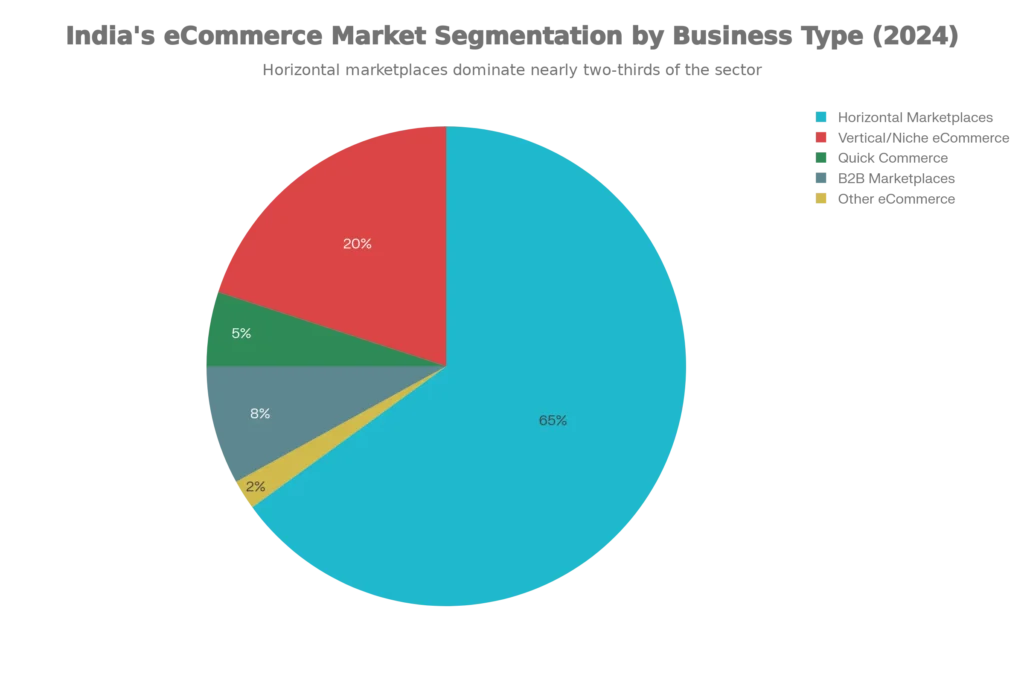

Tier 1: Horizontal Marketplaces

1. Flipkart

Flipkart remains the undisputed market leader in India’s eCommerce space, commanding 48% of the market share with a 2024 Gross Merchandise Value (GMV) of $24.7 billion. Founded as an India-first company, Flipkart has established itself as a cultural benchmark for online shopping in the country. The platform serves over 350 million registered users across more than 20,000 postal codes and operates through its proprietary logistics arm, Ekart, which ensures fast and reliable delivery.

Flipkart’s strength lies in its deep understanding of local consumer behavior, vernacular language support, and strong penetration in regional markets. The company operates across diverse categories including fashion, electronics, appliances, and home & lifestyle products. In FY25, Flipkart reduced its losses by 37%, demonstrating improving unit economics and a trajectory toward profitability. The platform continues to innovate through initiatives like Flipkart Minutes for quick commerce and a robust advertising network.

2. Amazon India

Amazon India holds the second position with an estimated 30-35% market share and a 2024 GMV of $22.7 billion. The global e-commerce giant entered India’s market with a premium positioning strategy, focusing on quality-conscious, urban customers and international selling opportunities. Amazon operates 100+ million registered customer accounts and maintains sophisticated logistics infrastructure spanning 15,000+ pin codes.

Amazon’s competitive advantages include its globally integrated supply chain, FBA (Fulfillment by Amazon) capabilities, and strong investment in customer trust infrastructure. The company reported EBITDA margins of 9.2% in FY25, answering critical questions about the long-term viability of eCommerce profitability in India. User growth at 13% year-on-year trails Flipkart, reflecting its more selective urban focus, but profitability metrics position Amazon as a stable, capital-efficient operator.

3. Myntra

As a fashion and lifestyle specialist, Myntra generated $9.8 billion GMV in 2024, securing the third position. Acquired by Flipkart in 2014, Myntra has evolved from a personalized gift platform (founded in 2007) into India’s dominant fashion eCommerce destination. The platform showcases the latest fashion and lifestyle brands and has experienced over 25% growth in app users year-on-year.

Myntra’s specialization in fashion allows hyper-targeted curation, exclusive brand partnerships, and trendy collections that appeal to style-conscious consumers. Operating as part of the Flipkart ecosystem, Myntra leverages shared logistics and customer base while maintaining distinct brand identity. The company achieved 7.4% EBITDA margins in FY25, demonstrating that category-focused specialization can yield profitability.

Tier 2: Vertical Specialists and Niche Leaders

4. Meesho

Meesho has emerged as India’s fastest-growing eCommerce company and a pioneer in social commerce. The platform has captured nearly 30% of India’s eCommerce market share through its revolutionary zero-commission model that democratizes online selling for small entrepreneurs and resellers. Founded on the principle of making eCommerce entrepreneurship accessible with minimal investment, Meesho enables sellers to reach customers through WhatsApp, Facebook, and Instagram.

What distinguishes Meesho is its focus on Tier II and Tier III cities and its enablement of small-scale entrepreneurs. The platform’s social-first approach leverages existing social networks and trust, reducing customer acquisition costs. With estimated GMV of $7-8 billion, Meesho represents a new business model that challenges the traditional commission-based marketplace structure.

5. BigBasket

BigBasket, now majority-owned by Tata Digital following Tata’s acquisition, operates as India’s leading online grocery platform with GMV exceeding $1 billion. The company pioneered scheduled grocery deliveries in India and continues to dominate the category with operations across 30+ cities. BigBasket has achieved EBITDA positivity post-acquisition, becoming a rare profitable eCommerce player in the grocery vertical.

The platform’s evolution demonstrates how category specialization and omnichannel integration (online + offline through Tata’s physical retail network) can create a defensible market position. BigBasket is expanding through BB Now, its quick commerce arm, indicating how traditional eCommerce leaders are adapting to emerging market segments.

6. FirstCry

FirstCry is India’s largest online marketplace for baby and kids’ products, serving over 10 million registered users with an estimated valuation exceeding $2 billion. Founded in 2010 and backed by SoftBank, FirstCry operates approximately 500+ physical franchise stores across major Indian cities, creating a true omnichannel experience. The company has achieved approximately 70% market share in online infant care products.

FirstCry’s model combines deep category expertise with physical retail presence, allowing customers to research online and purchase in-store or vice versa. This integrated approach has proven especially effective for parenting products, where trust and expert advice are paramount buying criteria. The company’s estimated GMV of $700 million (including offline) demonstrates the viability of niche vertical strategies in emerging eCommerce markets.

7. Nykaa

Nykaa, founded in 2012 by Falguni Nayar, has established itself as the leader in beauty, wellness, and fashion eCommerce with partnerships with 2,500+ national and international brands. The company became a pioneering eCommerce IPO in 2021, with founder Falguni Nayar’s family maintaining majority control. Nykaa operates over 100 physical stores across India, combining online and offline retail.

The company’s competitive advantage lies in its beauty-first curation, community engagement through blogs and tutorials, and guarantee of 100% genuine products. By focusing exclusively on beauty and wellness—categories with high customer lifetime value and lower return rates—Nykaa has built a loyal, primarily female customer base that generates strong repeat purchase behavior.

8. OLX India

OLX India dominates the used products and classifieds market with $3 billion GMV and an impressive 180 million annual unique visitors. As part of the global OLX Group (owned by Prosus), the company achieved 17% year-on-year revenue growth and a remarkable 213% year-on-year profit increase in recent periods. OLX India holds 37% market share in the used products category and 63% market share in used cars.

OLX’s evolution demonstrates the emergence of “recommerce”—the buying and selling of second-hand goods online. The company leverages AI-powered listing technology, smart suggestions, verified user infrastructure, and integrated financing options to simplify transactions. With 29% EBITDA margins and $2 billion annual revenue, OLX has proven the profitability of the classifieds model at scale.

9. AJIO

AJIO, launched by Reliance Retail in 2016, has become one of India’s most popular fashion eCommerce platforms, offering both local and international premium brands. The platform combines exclusive discounts with curated collections appealing to fashion-forward consumers. AJIO operates as part of Reliance’s broader digital commerce initiative, benefiting from the conglomerate’s retail infrastructure and supply chain.

The platform’s strength lies in its access to Reliance’s brand relationships, inventory integration with physical stores, and ability to offer premium fashion at competitive prices. AJIO’s omnichannel strategy allows customers to research online and purchase in nearby Reliance stores or order online for home delivery.

10. JioMart

JioMart, Reliance’s digital retail initiative, began by selling groceries but has expanded into lifestyle, fashion, and personal care products. The company’s innovative model integrates local kirana (neighborhood shop) partnerships, enabling small retailers to participate in digital commerce through Reliance’s platform. JioMart provides bulk buying discounts and leverages Reliance Retail’s extensive physical network for distribution.

JioMart represents a hybrid model that bridges digital commerce with traditional retail, particularly effective in smaller cities where kirana stores remain dominant. The integration of digital ordering with local fulfillment creates a unique value proposition for both consumers and small business partners.

11. Tata CLiQ

Tata CLiQ, launched in 2016 by the Tata Group, operates as an omnichannel eCommerce platform offering electronics, fashion, and lifestyle products. The platform leverages the Tata Group’s brand trust, supply chain infrastructure, and physical retail presence. Tata CLiQ offers seamless integration between online and offline channels, with options for store pickup (Click & Collect) and unified returns/service across channels.

The company’s advantages include association with the prestigious Tata brand, access to exclusive Tata products, and premium shopping experience through omnichannel integration. The platform operates 24/7 customer support and secured payment channels to enhance customer satisfaction.

12. Snapdeal

Snapdeal focuses on value-based shopping and affordability, targeting price-conscious consumers in Tier II and III cities. Founded in 2010, the platform maintains an extensive catalog of 15 million products across 750 categories, including electronics, fashion, home goods, and lifestyle items. Snapdeal’s positioning as an accessible marketplace for smaller cities differentiates it from Flipkart and Amazon, which have historically focused on metros.

The company continues to adapt to market dynamics through periodic special discounts and seasonal sales promotions. Snapdeal’s ability to serve price-sensitive consumers in non-metro markets has allowed it to maintain relevance despite competition from larger players expanding into smaller cities.

Tier 3: Emerging Quick Commerce Platforms

13. Blinkit

Blinkit, formerly known as Grofers, has pivoted to become the market leader in India’s quick commerce segment with approximately 45% market share. Founded in 2014, the company transformed its business model in 2021 to focus on ultra-fast delivery of groceries and daily essentials in 10-20 minutes. Blinkit operates hundreds of strategically placed dark stores (automated warehouses without retail presence) across major metropolitan areas.

The platform’s success demonstrates consumer demand for hyperlocal, instant-delivery services. Blinkit’s operational efficiency, achieved through optimized dark store networks and advanced logistics technology, has made it the market leader in quick commerce, despite intense competition from well-funded rivals.

14. Zepto

Zepto, founded in 2021 by Stanford University dropouts Aadit Palicha and Kaivalya Vohra, has emerged as the fastest-growing quick commerce startup with 21% market share. The company focuses on ultra-fast delivery of groceries and essential items through a hyper-local fulfillment model using micro-warehouses. Zepto’s rapid expansion and investor backing reflect strong market confidence in the quick commerce segment.

Zepto’s competitive positioning emphasizes speed (10-minute delivery guarantee), technological sophistication, and capital efficiency. The company’s ability to challenge established players like Blinkit demonstrates how focused execution on a specific problem can create rapid market traction.

15. Swiggy Instamart

Swiggy Instamart represents a major player’s diversification into quick commerce, leveraging Swiggy’s established food delivery logistics network. Operating with 27% market share in quick commerce, Swiggy Instamart delivers groceries and daily essentials within 15-30 minutes. The platform’s distinct advantage is its ability to leverage an existing fleet of delivery executives and established infrastructure across Indian cities.

By extending its delivery network from food to groceries and essentials, Swiggy has created operational synergies that reduce customer acquisition costs and improve logistics efficiency. This model demonstrates how established eCommerce or delivery platforms can efficiently move into adjacent categories.

Market Dynamics and Future Outlook

The Indian eCommerce sector is characterized by several important dynamics. First, the combined revenue of Flipkart, Amazon, and Myntra reached ₹56,700 crore in FY25, representing 17% year-on-year growth—a significant deceleration from the 50%+ CAGR growth witnessed during the sector’s earlier phases. This moderation reflects market maturation as penetration approaches 230 million users (17% of population), compared to China’s 60%.

Second, quick commerce has emerged as a disruptive force, already capturing 5% of eCommerce and potentially threatening growth in horizontal marketplaces through non-food category expansion. Leading horizontal players like Flipkart, Amazon, and Myntra are responding through their own quick commerce initiatives (Flipkart Minutes, Amazon Now, and M-Now), defending share in key metropolitan markets.

Third, profitability is becoming paramount. Amazon and Myntra achieved EBITDA margins of 9.2% and 7.4% respectively in FY25, demonstrating the viability of eCommerce economics at scale. This profitability focus contrasts with earlier venture-capital-backed models that prioritized growth over unit economics.

Fourth, the market is experiencing geographic expansion. Over 60% of eCommerce traffic now originates from beyond metros, indicating successful penetration into Tier II and Tier III cities. Companies like Meesho and Snapdeal have built substantial businesses precisely by serving these under-indexed markets.

The $147.3 billion market is projected to expand at 18.7% CAGR through 2028, with 400 million consumers by 2027. Profitability improvements, geographic expansion, and the rise of quick commerce and vertical specialists indicate a maturing ecosystem with multiple sustainable business models, rather than winner-take-all consolidation typical of earlier eCommerce markets.